Iron Condor Strategy - Margin Comparison vs Short Strangle (Indian Market Guide)

Introduction

Understanding Custom Algo Trading and Iron Condor is essential for modern market participants. Throughout this guide, we dive deep into Custom Algo Trading, Iron Condor, Short Strangle, Options Trading, Risk Management, highlighting how core concepts like Short Strangle and Options Trading shape consistent performance.

In our previous blog, we discussed the Short Strangle strategy and its margin implications. While Short Strangle offers high probability income, it carries unlimited risk and high margin requirements. The Iron Condor is a modified version of the Short Strangle that introduces defined risk and lower margin usage. In this guide, we'll cover what an Iron Condor is, how it differs from a Short Strangle, margin comparisons, risk-reward structure, and practical Nifty examples. Implementing an Iron Condor can be a highly efficient custom algo trading strategy.

What Is an Iron Condor?

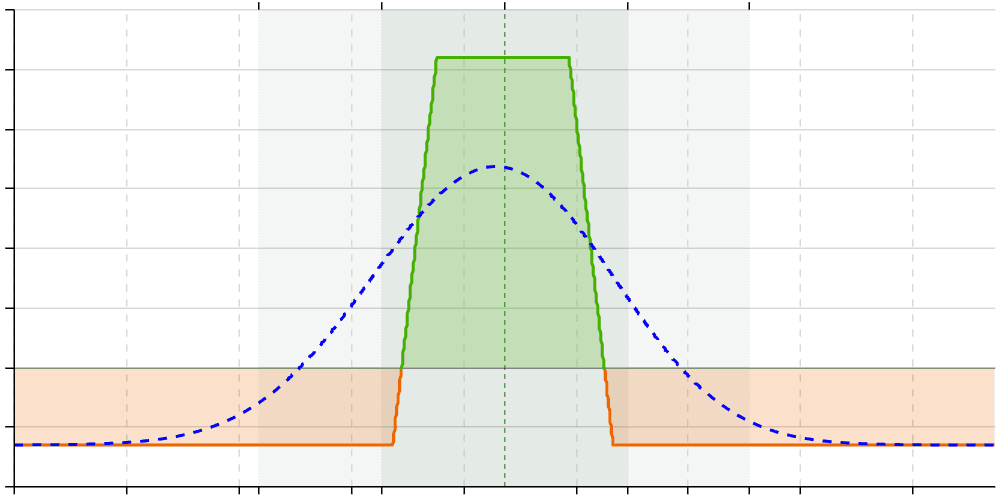

An Iron Condor is a hedged option selling strategy created by selling one OTM Call, buying a further OTM Call (hedge), selling one OTM Put, and buying a further OTM Put (hedge). All options have the same expiry. This converts unlimited risk into limited, defined risk. Automating such logic through custom algo trading ensures precise entry and execution.

Structure Example - Nifty Weekly Expiry

Assume Nifty Spot = 21,600. Trade Setup:

- Sell 21,900 Call @ ₹60

- Buy 22,100 Call @ ₹25

- Sell 21,300 Put @ ₹55

- Buy 21,100 Put @ ₹20

Net Premium Collected: (60 + 55) - (25 + 20) = ₹70. Lot size: 50. Maximum Profit = ₹70 × 50 = ₹3,500.

Margin Requirement Comparison

Short Strangle Margin: Approx ₹1.4 - ₹1.8 lakh per lot (unhedged, as on Feb-2026). Iron Condor Margin: Typically ₹40,000 - ₹70,000 per lot (depends on strike width & volatility). Why lower? Because buying protective options reduces worst-case risk, and SPAN calculates margin based on maximum possible loss. Effective custom algo trading systems can dynamically calculate and monitor these margins.

Risk-Reward Profile

Maximum Profit: Limited to net premium received. Maximum Loss: Defined and limited. Example: Strike gap = 200 points. Max loss = 200 - 70 = 130 points. 130 × 50 = ₹6,500.

Break-even Points

Upper BE = Short Call Strike + Net Premium. Lower BE = Short Put Strike - Net Premium.

When Does Iron Condor Work Best?

- Sideways markets

- Volatility contraction

- After event-based IV spikes

- Weekly expiry range trades

Want us to build this for you?

Talk to our teamWhen Does It Fail?

- Strong trending markets

- Volatility expansion

- Narrow strike selection

Iron Condor vs Short Strangle (Quick Comparison)

- Risk: Short Strangle - Unlimited | Iron Condor - Limited

- Margin: Short Strangle - High | Iron Condor - Lower

- Capital Required: Short Strangle - Large | Iron Condor - Moderate

- Suitable For: Short Strangle - Experienced traders | Iron Condor - Retail traders

Final Thoughts

Iron Condor is not "better" than Short Strangle - it is simply a capital-efficient and risk-defined variation. Serious traders focus not only on premium collection, but on margin utilization, worst-case scenarios, volatility behavior, and risk-adjusted return. Incorporating these sophisticated checks into custom algo trading software provides an edge for retail and seasoned traders alike.

"Disclaimer: This article is for educational purposes only and not investment advice."

Already Have a Strategy? Let's Automate It.

At Arkalogi, we convert your trading logic into fully automated systems - integrated with your broker, backtested on real market data, and deployed on a live server. You describe your strategy in plain English. We handle everything else. Book a free honest assessment on WhatsApp to chat with us. No sales pitch. Just clarity on what's possible and what infrastructure you need to avoid common failure modes.

This post was written by Rina Sethi, a Algo Trading Developer at Arkalogi.

If you want a custom strategy like this built for your broker, we can help.

Relevant Service

This post is relevant to our expertise in Custom Trading Strategy Development.

See service→Share this article

Related Articles

Most Popular Algorithmic Trading Strategies (and When They Work)

From trend-following to market making, here's what each strategy category needs, where it shines, and why risk controls matter more than entries.

Short Strangle Options Strategy - Margin, Risk & Practical Indian Market Example

The Short Strangle is one of the most popular option selling strategies used by traders in Indian markets. It is simple in structure, works well in range-bound markets, and benefits from time decay.

Build vs. Buy: Should You Develop Custom Algotrading Software or Use Off-the-Shelf Tools?

Every successful trader hits this fork in the road. Should you subscribe to ready-made tools or build custom software? We break down the costs, risks, and advantages.